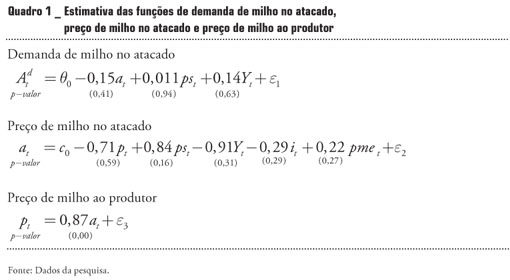

The objective of this paper is to understand the dynamics of the Brazilian corn market by investigating the main factors affecting volumes and prices. Unit roots tests were taken using the DF-GLS - Dickey Fuller Generalized Least Square methodology, and Johansen's co-integration tests (1988). The estimated model for price adjustment was a Self-Regression Vector Error Correction Model - VEC, with identification by the Sims-Bernanke procedure. We conclude that there is a significant interaction between the corn and the soybean markets, which present a complementary relationship on the supply side and substitution relationship on the demand side. Additionally, we conclude that macroeconomic factors such as income and interest rates are important in determining corn prices for producers and on the wholesale market. It should be noted that external grain prices play a relatively important role in formation of domestic corn prices.

corn; soybean; price; time series