Abstract

Paper aims

The purpose of this article is to identify the research opportunities in capital budgeting.

Originality

This research contributes to the literature by providing a methodology where researchers can potentially identify gaps from budgeting according to the existing scientific literature and contributes to the engineering management practice by to identifying the difficulties found by engineering managers that interfere in the capital budgeting process.

Research method

It was used the Knowledge Development Process-Constructivist (Proknow-C) tool that can researchers potentially identify gaps from budgeting according to the existing scientific literature. It then explicitly define the frontiers of knowledge and possible opportunities to follow when investigating the field.

Main findings

Capital budgeting is not shown as a macro research area for the researchers. Few authors have developed research with the same scopes or few of them still research on the theme.

Implications for theory and practice

The academy advocates that capital budgeting has a key role in business management and, therefore, managers have to use more sophisticated analysis practices. Organizations should seek professionals with experience in capital projects appraisal and who are familiar with and knowledgeable in the use of adequate practices for decision-making.

Keywords:

Budgeting; Practices capital budgeting; Engineering managers; Scientific production

1. Introduction

Capital budgeting is one of the most important decisions faced by the financial management of any organization (Batra & Verma, 2014Batra, R., & Verma, S. (2014). An empirical insight into different stages of capital budgeting. Global Business Review, 15(2), 339-362. http://dx.doi.org/10.1177/0972150914523588.

http://dx.doi.org/10.1177/09721509145235...

). It is a planning mechanism used by an organization to make evaluation decisions on how to allocate resources among investment projects (Al-Mutairi et al., 2018Al-Mutairi, A., Naser, K., Saeid, M., & McMillan, D. (2018). Capital budgeting practices by non-financial companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance, 6(1), 2-18. http://dx.doi.org/10.1080/23322039.2018.1468232.

http://dx.doi.org/10.1080/23322039.2018....

) and assessing the investment projects that will create benefits for periods of over one year and that will assist the company to obtain revenues or reduce future costs (Khamees et al., 2010Khamees, B. A., Al-Fayoumi, N., & Al-Thuneibat, A. A. (2010). Capital budgeting practices in the Jordanian industrial corporations. International Journal of Commerce and Management, 20(1), 49-63. http://dx.doi.org/10.1108/10569211011025952.

http://dx.doi.org/10.1108/10569211011025...

).

Capital budgeting is a tool that can be used for very simple operational decisions such as equipment replacement or more complex strategies such as the construction of a new plant (Leon et al., 2008Leon, F. M., Isa, M., & Kester, G. W. (2008). Capital budgeting practices of listed Indonesian companies. Asian Journal of Business and Accounting, 1(2), 175-192.). In any case, when considering the importance of capital investment decisions, it is imperative that managers use the appropriate practice to ensure a sound decision (Toit & Pienaar, 2005Toit, M. J. D., & Pienaar, A. (2005). A review of the capital budgeting behaviour of large South African firms. Meditari Accountancy Research, 13(1), 19-27. http://dx.doi.org/10.1108/10222529200500002.

http://dx.doi.org/10.1108/10222529200500...

).

More sophisticated capital budgeting practices are Discounted Cash Flow (DFC) practices that take into account the value of money over time, namely: Net Present Value (NPV), Internal Rate of Return (IRR). Among the simplest are Payback (PB) and Accounting Return Rate (ARR) (Leon et al., 2008Leon, F. M., Isa, M., & Kester, G. W. (2008). Capital budgeting practices of listed Indonesian companies. Asian Journal of Business and Accounting, 1(2), 175-192.; Brijlal & Quesada, 2009Brijlal, P., & Quesada, L. (2009). The use of capital budgeting techniques in businesses: a perspective from the Western Cape. Journal of Applied Business Research, 25(4), 37-46.; Hall & Mutshutshu, 2013Hall, J. H., & Mutshutshu, T. (2013). Capital budgeting techniques employed by selected South African state-owned companies. Corporate Ownership and Control, 10(3), 177-187. http://dx.doi.org/10.22495/cocv10i3c1art2.

http://dx.doi.org/10.22495/cocv10i3c1art...

).

The interest in understanding the capital budgeting practices used by companies was first observed in the beginning of the 1960s. Evidence from the 60s and 70s reflected a certain managerial trend to gradually use models that were theoretically superior based on discounted cash flows (Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

). The fields of engineering economics and finance have long stories of research on how to choose an interest rate for an investment project or capital budgeting problem (Eschenbach & Cohen, 2006Eschenbach, T., & Cohen, R. (2006). Which interest rate for evaluating projects? Engineering Management Journal, 18(3), 11-19. http://dx.doi.org/10.1080/10429247.2006.11431699.

http://dx.doi.org/10.1080/10429247.2006....

).

According to Mao (1970)Mao, J. C. T. (1970). Survey of capital budgeting: theory and practice. The Journal of Finance, 25(2), 349-360. http://dx.doi.org/10.1111/j.1540-6261.1970.tb00513.x.

http://dx.doi.org/10.1111/j.1540-6261.19...

, since the 60s, the literature on capital budgeting has been characterized by an increase in the application of such analytical techniques. There are modern budgeting techniques that can be used in investment decision making, but managers seem not to have adopted new techniques at a large scale.

The literature still tries to explain why the gap between what is indicated by the theory and what is actually practiced still exists (Bennouna et al., 2010Bennouna, K., Meredith, G. G., & Marchant, T. (2010). Improved capital budgeting decision making: evidence from Canada. Management Decision, 48(2), 225-247. http://dx.doi.org/10.1108/00251741011022590.

http://dx.doi.org/10.1108/00251741011022...

). Most explanations are related to the culture, preferences and limitations of the managers (for example, Hall & Millard, 2011Hall, J., & Millard, S. (2011). Capital budgeting practices used by selected listed South African firms. South African Journal of Economic and Management Sciences, 13(1), 85-97. http://dx.doi.org/10.4102/sajems.v13i1.200.

http://dx.doi.org/10.4102/sajems.v13i1.2...

; Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

; Souza & Lunkes, 2016Souza, P., & Lunkes, R. J. (2016). Capital budgeting practices by large Brazilian companies. Contaduría y Administración, 61(3), 514-534. http://dx.doi.org/10.1016/j.cya.2016.01.001.

http://dx.doi.org/10.1016/j.cya.2016.01....

). While various methods have been proposed in the literature, subjective approaches have gained less attention (Toloo et al., 2018Toloo, M., Nalchigar, S., & Sohrabi, B. (2018). Selecting most efficient information system projects in presence of user subjective opinions: a DEA approach. Central European Journal of Operations Research, 26(4), 1027-1051. http://dx.doi.org/10.1007/s10100-018-0549-4.

http://dx.doi.org/10.1007/s10100-018-054...

).

Thus, it notes that this gap must be better studied and exploited. For this reason, the purpose of this article is to construct a systematic analysis of capital budgeting literature. In these terms, it is intended to answer these questions: Who are the authors and journals in the area that stand out most in the scientific environment? What are the possibilities for research in capital budgeting?

This work identifies existing gaps that could become future research that contributes to scientific and practical terms to the capital budgeting process based on a systematic analysis of the international literature review. It is believed that gathering information into a single material (i) a process to identify and select capital budgeting articles; (ii) a bibliometric analysis of the relevant publications on this topic; and (iii) a systematic analysis of the articles of bibliographic portfolio be useful for researchers and professionals to prioritize their efforts to those researches that generate scientific and practical contributions, based on the knowledge generated and presented reflections.

2. Capital budgeting

Capital budgeting refers to the financial assessment of the capital investment proposals of a company (Al-Mutairi et al., 2018Al-Mutairi, A., Naser, K., Saeid, M., & McMillan, D. (2018). Capital budgeting practices by non-financial companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance, 6(1), 2-18. http://dx.doi.org/10.1080/23322039.2018.1468232.

http://dx.doi.org/10.1080/23322039.2018....

). In other words, capital budgeting involves assessing whether the future cash flows resulting from a suggested investment justify whether it should be made, considering the risks and uncertainties (Leon et al., 2008Leon, F. M., Isa, M., & Kester, G. W. (2008). Capital budgeting practices of listed Indonesian companies. Asian Journal of Business and Accounting, 1(2), 175-192.).

Budgeting is considered as one of the most important decisions faced by the financial manager (Ryan & Ryan, 2002Ryan, P. A., & Ryan, G. P. (2002). Capital budgeting practices of the Fortune 1000: how have things changed? Journal of Business and Management, 8(4), 1-15.). The efficiency of the capital budgeting process of an organization and the respective financial analysis methods depend, ultimately, on how it influences the behavior of the managers to allocate scarce resources across competing investment alternatives (Pike, 1988Pike, R. H. (1988). An empirical study of the adoption of sophisticated capital budgeting practices and decision-making effectiveness. Accounting and Business Research, 18(72), 341-351. http://dx.doi.org/10.1080/00014788.1988.9729381.

http://dx.doi.org/10.1080/00014788.1988....

; Pike & Ooi, 1988Pike, R. H., & Ooi, T. S. (1988). The impact of corporate investment objectives and constraints on capital budgeting practices. The British Accounting Review, 20(2), 159-173. http://dx.doi.org/10.1016/0890-8389(88)90038-8.

http://dx.doi.org/10.1016/0890-8389(88)9...

).

When making investment decisions, the managers make a series of subjective calls (Pike, 1983Pike, R. H. (1983). A review of recent trends in formal capital budgeting processes. Accounting and Business Research, 13(51), 201-208. http://dx.doi.org/10.1080/00014788.1983.9729753.

http://dx.doi.org/10.1080/00014788.1983....

). Also, the profile of the managers is considered as a factor that may influence capital budgeting practices used by the companies (Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

). In addition, different organizations use different decision-makers to adopt the decisions related to the referred budgeting (Brijlal & Quesada, 2009Brijlal, P., & Quesada, L. (2009). The use of capital budgeting techniques in businesses: a perspective from the Western Cape. Journal of Applied Business Research, 25(4), 37-46.).

Firstly, the capital investment decision significantly influences the growth rate of an organization; making a wrong decision may ruin the company. Secondly, such decisions require large amounts of funds. Finally, they are amongst the most complex decisions in terms of uncertainties in relation to future cash flow estimations, as well as in relation to the social, technological, economic and political impacts on the estimations, which increases their complexity (Egbide et al., 2013Egbide, B., Uwalomwa, U., & Agbude, G. A. (2013). Capital budgeting, government policies and the performance of SMEs in Nigeria: a hypothetical case analysis. IFE PsychologIA, 21(1), 55-73.).

Assessing the capital budgeting proposals is part of the decision to make investments (Arnold & Hatzopoulos, 2000Arnold, G. C., & Hatzopoulos, P. D. (2000). The theory-practice gap in capital budgeting: evidence from the United Kingdom. Journal of Business Finance & Accounting, 27(5-6), 603-626. http://dx.doi.org/10.1111/1468-5957.00327.

http://dx.doi.org/10.1111/1468-5957.0032...

). Within that context, the financial management and the capital investment decision-making are fundamental for the survival and success of the company in the long term (Bennouna et al., 2010Bennouna, K., Meredith, G. G., & Marchant, T. (2010). Improved capital budgeting decision making: evidence from Canada. Management Decision, 48(2), 225-247. http://dx.doi.org/10.1108/00251741011022590.

http://dx.doi.org/10.1108/00251741011022...

).

Additionally, capital budgeting covers the most fundamental financial decision of any organization, whether it is a small, medium or large-sized company, since it determines its profitability and success (Egbide et al., 2013Egbide, B., Uwalomwa, U., & Agbude, G. A. (2013). Capital budgeting, government policies and the performance of SMEs in Nigeria: a hypothetical case analysis. IFE PsychologIA, 21(1), 55-73.). Such relevance justifies why different organizations use different capital budgeting practices and procedures and how they operate complex interdependence networks among the budgeting variables (Pike, 1986Pike, R. H. (1986). The design of capital-budgeting processes and the corporate context. Managerial and Decision Economics, 7(3), 187-195. http://dx.doi.org/10.1002/mde.4090070307.

http://dx.doi.org/10.1002/mde.4090070307...

).

Considering that there are different ways in which the efficiency of the decisions may be improved (for example, qualification, recruiting incentives, etc.), the capital budgeting techniques and procedures are seen as important aspects in that sense (Pike, 1989Pike, R. H. (1989). Do sophisticated capital budgeting approaches improve investment decision-making effectiveness? The Engineering Economist, 34(2), 149-161. http://dx.doi.org/10.1080/00137918908902983.

http://dx.doi.org/10.1080/00137918908902...

).

Capital budgeting has been a subject of growing theoretical and empirical research in the finance literature (Al-Mutairi et al., 2018Al-Mutairi, A., Naser, K., Saeid, M., & McMillan, D. (2018). Capital budgeting practices by non-financial companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance, 6(1), 2-18. http://dx.doi.org/10.1080/23322039.2018.1468232.

http://dx.doi.org/10.1080/23322039.2018....

). The central issue in this literature is to explore the most frequently used practices and the reason behind using some techniques more frequently than others (Block, 1997Block, S. (1997). Capital budgeting techniques used by small business firms in the 1990s. The Engineering Economist, 42(4), 289-302. http://dx.doi.org/10.1080/00137919708903184.

http://dx.doi.org/10.1080/00137919708903...

; Ryan & Ryan, 2002Ryan, P. A., & Ryan, G. P. (2002). Capital budgeting practices of the Fortune 1000: how have things changed? Journal of Business and Management, 8(4), 1-15.; Markovics, 2016Markovics, K. S. (2016). Capital budgeting methods used in some European countries and in the United States. Universal Journal of Management, 4(6), 348-360. http://dx.doi.org/10.13189/ujm.2016.040604.

http://dx.doi.org/10.13189/ujm.2016.0406...

).

Empirical research provided inconclusive evidence regarding the capital budgeting practices among practitioners; while several researches showed the payback period (PP) as the most popular technique employed in evaluating projects, other investigations demonstrated that discounted cash-flows practices are the most frequently used capital budgeting techniques (for example Sandahl & Sjögren, 2003Sandahl, G., & Sjögren, S. (2003). Capital budgeting methods among Sweden’s largest groups of companies: the state of the art and a comparison with earlier studies. International Journal of Production Economics, 84(1), 51-69. http://dx.doi.org/10.1016/S0925-5273(02)00379-1.

http://dx.doi.org/10.1016/S0925-5273(02)...

; Hall & Mutshutshu, 2013Hall, J. H., & Mutshutshu, T. (2013). Capital budgeting techniques employed by selected South African state-owned companies. Corporate Ownership and Control, 10(3), 177-187. http://dx.doi.org/10.22495/cocv10i3c1art2.

http://dx.doi.org/10.22495/cocv10i3c1art...

; Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

).

3. Methodological procedures

A systematic review is a means of evaluating and interpreting all available research relevant to a specific research question, topic area, or phenomenon of interest. Its aim to present an evaluation of an investigation topic by using a trustworthy and rigorous methodology (Kitchenham, Brereton, Budgen, Turner, Bailey, and Linkman). The systematic review of literature is defined as by the manner in which the reviewer proceeds, stage by stage, with full transparency and explicitness about what is done, typically using a protocol to guide the process (Young et al., 2002Young, K., Ashby, D., Boaz, A., & Grayson, L. (2002). Social science and the evidence-based policy movement. Social Policy and Society, 1(3), 215-224. http://dx.doi.org/10.1017/S1474746402003068.

http://dx.doi.org/10.1017/S1474746402003...

).

Pittaway et al. (2004)Pittaway, L., Robertson, M., Munir, K., Denyer, D., & Neely, A. (2004). Networking and innovation: a systematic review of the evidence. International Journal of Management Reviews,5-6(3-4), 137-168. http://dx.doi.org/10.1111/j.1460-8545.2004.00101.x.

http://dx.doi.org/10.1111/j.1460-8545.20...

proposed a comprehensive and detailed process to arrive at organized results from a large potential sample of articles. However, the origin of the criteria for content analysis was not explicit. Kitchenham et al. (2009)Kitchenham, B., Brereton, O. P., Budgen, D., Turner, M., Bailey, J., & Linkman, S. (2009). Systematic literature reviews in software engineering: a systematic literature review. Information and Software Technology, 51(1), 7-15. http://dx.doi.org/10.1016/j.infsof.2008.09.009.

http://dx.doi.org/10.1016/j.infsof.2008....

proposed a subjective process for choosing articles in specific journals. But, Ensslin et al. (2010)Ensslin, L., Ensslin, S. R., Lacerda, R. T. O., & Tasca, J. E. (2010). Proknow-C, Knowledge Development Process-Constructivist: processo técnico com patente de registro pendente junto ao INPI. Florianópolis. presented the Proknow-C, a detailed and comprehensive process for selecting a large sample of potential articles with the integration of criteria grounded in a worldview, which enables a holistic view of the analysis.

Proknow-C presents a structured process to build knowledge about the researcher interest area, according to the constructivist view. The methodology consists of a series of sequential procedures that begin with the definition of the search engine for scientific articles to be used, followed by pre-established processes of filtering and the selection of a relevant bibliographic portfolio (Ensslin et al., 2010Ensslin, L., Ensslin, S. R., Lacerda, R. T. O., & Tasca, J. E. (2010). Proknow-C, Knowledge Development Process-Constructivist: processo técnico com patente de registro pendente junto ao INPI. Florianópolis.).

Proknow-C is a set of steps or guides to filter and analyze the bibliographic information on a certain theme or subject. It is subdivided into four stages: 1) the selection of the bibliographical portfolio; 2) the bibliometric analysis of the selected articles; 3) the systematic analysis of the selected articles; and 4) the definition of the research question and the research objective (Waiczyk & Ensslin, 2013Waiczyk, C., & Ensslin, E. R. (2013). Avaliação de produção científica de pesquisadores: mapeamento das publicações científicas. Revista Contemporânea de Contabilidade, 10(20), 97-112. http://dx.doi.org/10.5007/2175-8069.2013v10n20p97.

http://dx.doi.org/10.5007/2175-8069.2013...

). The selection of the articles is a singular process, subject to restriction researchers' limitations, according to the theme that they want to study. The limitations of this process are as follows: the keyword definition by the researchers; the identification of the number of citations per article through Google Scholar; and the analysis of the article's title, summary and full text, according to the researchers' preferences (Lacerda et al., 2016Lacerda, R. T. O., Ensslin, L., Ensslin, S. R., Knoff, L., & Dias Junior, C. M. (2016). Research Opportunities in business process management and performance measurement from a constructivist view. Knowledge and Process Management, 23(1), 18-30. http://dx.doi.org/10.1002/kpm.1495.

http://dx.doi.org/10.1002/kpm.1495...

).

3.1. Bibliographic portfolio selection

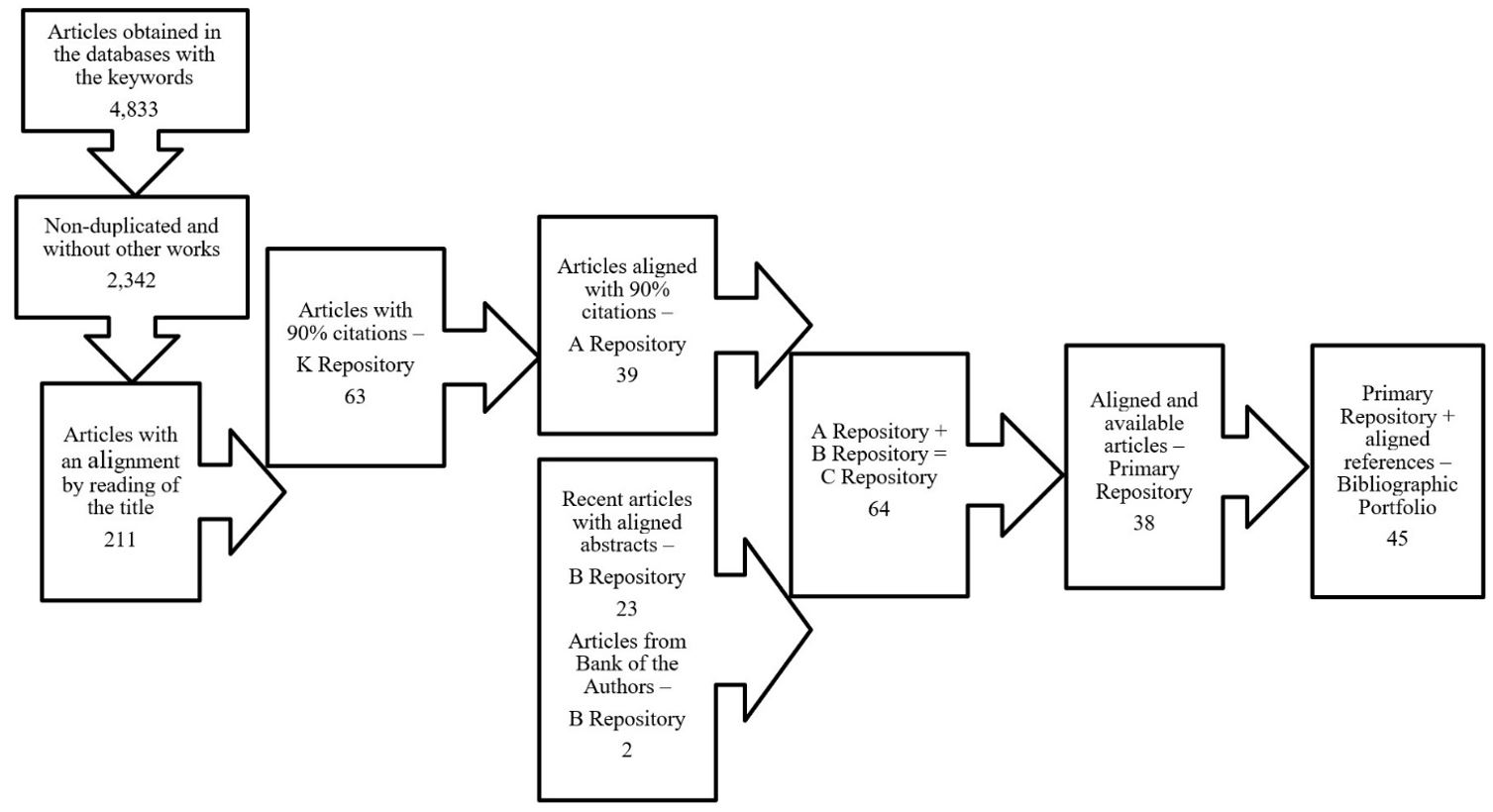

The first stage involves selecting the articles that constitute the bibliographic portfolio (BP). Selecting the portfolio requires: i) defining the keywords for the research axis; ii) selecting the databases; iii) searching for the articles on the selected databases, and iv) testing the adherence of the keywords.

Defining the keywords (KW) for this research involves the theme of capital budgeting and, therefore, only one axis is involved according to Proknow-C. The axis allows the researcher to target the construction of the necessary knowledge of its context. Since capital budgeting involves assessing long-term investment projects, “investment budget” and “investment appraisal” are also used as keywords.

Moreover, there is a variation in the KW used by researchers. To cover all the words with different terminologies, they were used expressions with Asterisk, e.g. “capital budget*”, “investment* budget*” and “investment* appraisal”. The Boolean expression “or” is used in databases to select the articles that have either keyword.

The search for the articles in seven databases (EBSCO Academic Search Premier, ISI Web of Science, Emerald Insight, Science Direct, Scopus – Elsevier, Wiley Online Library and Scientific Periodicals Electronic Library – SPELL). The publication period was restricted up to December 2017.

After the implementation of the articles, the analysis of the adherence of KWs occurred. This step analysed if the used KWs are the same as those used by researchers to address the issue.

According to the process, the keywords of five articles selected at random were checked (Ensslin et al., 2010Ensslin, L., Ensslin, S. R., Lacerda, R. T. O., & Tasca, J. E. (2010). Proknow-C, Knowledge Development Process-Constructivist: processo técnico com patente de registro pendente junto ao INPI. Florianópolis.). The objective is to validate the 3,815 total articles found by the search in the seven databases. If the words used in the selected articles are equivalent to those used in the search of the articles, the adherence was confirmed. If there are new words, the search must be redone. The titles of articles were read and analysed so that the three keywords were evaluated for adherence to the theme of the use of capital budgeting.

Through the analysis of the five articles, nineteen different keywords were identified among them. There are keywords used in databases. “Capital budgeting” and “Investment Appraisal” confirm the adherence to the theme of capital budgeting. The phrases “Cost of capital”, “Payback Period”, “Internal Rate of Return”, “Net Present Value”, “WACC”, “Real options”, “Discount rate”, “Risk”, “Capital budgeting practices”, “Risk in capital budgeting”, and “Sensitivity analysis in capital budgeting” are related to the methods used in the capital budgeting process. Since the goal is to build a general theoretical framework of the theme, keyword specific about capital budgeting practices were not used in searches.

It is assumed that there is convergence between the keywords set for conducting the process and the keywords used by the researchers of the articles in the Gross Articles Database. That is, the authors often use the keywords “Capital budgeting” and “Investment Appraisal” when they develop research on capital budgeting.

A total of 4,833 articles were found, and they were filtered according to their redundancy, title alignment, scientific acknowledgement and abstract alignment (Waiczyk & Ensslin, 2013Waiczyk, C., & Ensslin, E. R. (2013). Avaliação de produção científica de pesquisadores: mapeamento das publicações científicas. Revista Contemporânea de Contabilidade, 10(20), 97-112. http://dx.doi.org/10.5007/2175-8069.2013v10n20p97.

http://dx.doi.org/10.5007/2175-8069.2013...

). 2.342 redundant references were identified and excluded. Redundancy happens because the same article can be indexed in more than one database. Thus, when filtering different databases, the same article can be selected more than once, so it is necessary to eliminate it in the filtering. Also, 26 53 book sections and 198 duplicate articles that had not been identified by the EndNote software were excluded. Subsequent to the elimination of these references, the Gross Articles Database presented a total of 2,214 articles that were submitted to the analysis of alignment by reading of the title.

At that moment, the 2,214 articles were read and the alignment of each of them was verified in relation to the research topic. It can be seen that the process resulted in 211 articles with titles properly aligned, and 2,003 were eliminated at this stage because they were considered misaligned. Titles such as “Economic evaluation of short rotation coppice systems for energy from biomass”, “Life cycle costing: evaluating its use in UK practice” and “State highway capital expenditure and the economic cycle” were eliminated and “Capital budgeting under conditions of uncertainty”, Investment Decisions on Long-term Assets: Integrating Strategic and Financial Perspectives” and “Investment appraisal techniques and constraints on capital investment” were considered aligned.

The 211 articles with aligned titles were submitted to a scientific recognition test. This test aims to verify the potential of the article for the composition of the bibliographic portfolio, that is, how much it is referenced by authors who deal with capital budget. To evaluate this recognition before the academic community, the amount of citations of each article in the Google Scholar platform was checked. The number of citations of the 211 was manually collected.

After assessing the scientific recognition, the data of the articles were organized in descending order according to the number of citations. In this database, the percentage of representativeness of the citations was calculated in relation to the total of 5,478. From the calculation of the cumulative percentage, a cutoff point was defined in 90% of the total citations, which corresponds to 63 articles with 17 or more citations. Such a cut is defined by the researcher (Marafon et al., 2015Marafon, A. D., Ensslin, L., Lacerda, R. T. O., & Ensslin, S. R. (2015). The effectiveness of multi-criteria decision aid methodology. European Journal of Innovation Management, 18(1), 86-109. http://dx.doi.org/10.1108/EJIM-10-2013-0106.

http://dx.doi.org/10.1108/EJIM-10-2013-0...

). The 63 articles were incorporated into the “K Repository”.

The selection of the 63 articles is justified since together they have a total of 4,941 citations, while the 148 totals only 537 citations.

The 148 articles that have 10% of the citations, that is, have scientific recognition below to the cutoff point or not yet confirmed for being recent and have not received quotations from the scientific community. Such articles were incorporated into the “P Repository”.

The reading of the 63 abstracts allowed to identify 39 aligned to the theme and that were incorporated into the “A Repository”. These articles have scientific recognition and have title and abstract aligned. The remaining 24 articles with non-adherent abstracts were deleted.

Authors and co-authors were selected from the 39 articles in “A Repository”, with the purpose of composing the “Bank of authors”. This bank is used to verify if the articles in the “P Repository” were developed by authors of “A Repository”, since the authors of the latter may have a scientific trajectory of studies about the capital budget.

It was noticed that 63 different researchers compose “A Repository”. It is therefore possible that articles in the “P Repository” have been written by those authors or have not been cited in other research since their publication. Therefore, recent articles or authors of the “Bank of authors” need to be analyzed.

In order to avoid relevant articles being discarded from the bibliographic portfolio, the analysis of the articles in the “P Repository” is to verify if there is any article without scientific recognition recently published. Thus, articles published in 2013 until 2017 were considered recent.

It was verified that 35 recent articles of the “P Repository” have been found. Thus, the abstracts of these articles were read, to verify the possible alignment to the subject under study. In this stage, 23 articles with aligned summary were identified and added to “B Repository”. In this way, it can be observed that the other 12 recent articles were considered to be misaligned to the research topic and, therefore, do not belong to “B Repository”.

In addition, the authors and co-authors of the 113 non-recent articles were analyzed to verify if they belong to the “Bank of authors” and 6 articles were identified. The abstracts of the six articles were read and the adherence to the research theme was verified. We found 2 articles aligned and added to “B Repository”. The articles were “Measuring the use of capital budgeting techniques with the postal questionnaire - the UK perspective” by Rogers W. Mills and Richard H. Pike's “The impact of corporate investment objectives and constraints on capital budgeting practices”.

Thus, “B Repository” consisted of 25 articles, of which 23 are recent and 2 are from the “Bank of authors”. Finally, the 39 articles in “A Repository” and the 25 articles in “B Repository”, which gave rise to “C Repository”, are combined. This repository has 64 articles with title and abstract aligned.

The last stage of the filtering of the raw articles bank comprises the analysis of the gratuity and integral availability and complete reading of the articles. In this line, the 48 articles of “C Repository” were available and free of charge through the CAPES Periodicals Portal, Google Academic or databases of periodicals signed by the Library of the Federal University of Santa Catarina.

It was found that 64 articles were available completely and free of charge. From the full reading, it was found that 38 discussed, from some perspective, the use of the capital budgeting. These articles were considered aligned and were therefore kept in the “Primary Repository”.

To finalize the process of construction of the bibliographic portfolio, the bibliographic references that were used by the authors of the 38 primary articles are analyzed.

Thus, the references of the articles were compiled, totaling 879 in the References Database. Firstly, 369 were identified and eliminated from redundant references or from conferences, books, and other sources. The References Database without duplicity presented a total of 399 articles, which were submitted to the analysis regarding alignment of title.

Then, the alignment of the title of 87 articles with the theme of the research was verified. The 87 articles with aligned titles were submitted to the scientific recognition test. After assessing the scientific recognition, the data of the articles were ordered in descending order according to the number of citations. The percentage of representativeness of the citations was calculated in relation to the total of 7,190. From the calculation of the cumulative percentage, a cut-off point was defined in 80% of the total citations, which corresponds to 33 articles with 76 or more citations.

The abstracts of the 26 articles were read, since 9 were already in the primary portfolio, and there were 12 adherents to the research theme. However, it has been found that only 9 are available in full and free of charge. In this way, the complete reading was performed and it was verified that 7 are aligned with the research theme.

This concludes the construction of the Bibliographic Portfolio. It is constituted by 45 articles, 38 of them originate from the primary portfolio and 7 from their references. The articles database filtering is demonstrated in Figure 1.

3.2. Bibliometric analysis

The second stage of the process involves the bibliometric analysis. The referred analysis involves the quantitative and qualitative study of the characteristics of the 45 articles in the portfolio and the 80 references with aligned titles (eliminating the articles inserted in the portfolio during the representativity stage).

The bibliometric analysis encompasses i) researchers with a history in the area of knowledge; and ii) journals that have devoted some space for publications on the subject.

Firstly, we identified the keywords used by researchers to represent the subject of research. A total of 84 keywords were used in the BP articles and 79 in the BP references. The most prominent keyword is “capital budgeting”, used by 9 BP articles and 7 references.

The keyword “investment appraisal” was used in reference articles. Other words such as “investments”, “project” and “practices” were used. This denotes that the words used to select raw articles are aligned as they are employed by the area's researchers.

The 45 articles of BP are constituted by 72 authors, while the aligned references are constituted by 122. Within the portfolio there are authors who have published more than one of the selected articles. In the same way in the references there are authors who were cited more than once among the 45 articles in the portfolio. Among the 72 authors, two are highlighted.

The most prominent one with seven articles in BP is Pike, R. H. (Pike, 1983Pike, R. H. (1983). A review of recent trends in formal capital budgeting processes. Accounting and Business Research, 13(51), 201-208. http://dx.doi.org/10.1080/00014788.1983.9729753.

http://dx.doi.org/10.1080/00014788.1983....

, 1984Pike, R. H. (1984). Sophisticated capital budgeting systems and their association with corporate performance. Managerial and Decision Economics, 5(2), 91-97. http://dx.doi.org/10.1002/mde.4090050207.

http://dx.doi.org/10.1002/mde.4090050207...

, 1986Pike, R. H. (1986). The design of capital-budgeting processes and the corporate context. Managerial and Decision Economics, 7(3), 187-195. http://dx.doi.org/10.1002/mde.4090070307.

http://dx.doi.org/10.1002/mde.4090070307...

, 1989Pike, R. H. (1989). Do sophisticated capital budgeting approaches improve investment decision-making effectiveness? The Engineering Economist, 34(2), 149-161. http://dx.doi.org/10.1080/00137918908902983.

http://dx.doi.org/10.1080/00137918908902...

; Pike & Ooi, 1988Pike, R. H., & Ooi, T. S. (1988). The impact of corporate investment objectives and constraints on capital budgeting practices. The British Accounting Review, 20(2), 159-173. http://dx.doi.org/10.1016/0890-8389(88)90038-8.

http://dx.doi.org/10.1016/0890-8389(88)9...

), a finance and accounting professor at the School of Management at the University of Bradford, United Kingdom. Pike, R. H. conducts investigations in the areas of investment and risk, credit management, investment in new technologies, strategic management accounting and intellectual capital. The publications on capital budgeting are mostly from the 80s and 90s. This does not mean that the author does not have a history in the area, since he wrote many of the articles on the theme. It only means that his current research focus is not capital budgeting.

Pike, R. H. has four articles in the references, and he is the second most prominent author along with Kester, G. W. This shows that Pike, R. H. has a history of researching capital budgeting before the rest of the scientific community.

It may also be observed that the prominent authors are specialists in the area of investment and risk, finance, financial management and capital budgeting. Since this theme is discussed within the area of finance, capital budgeting is not shown as a macro research area for the authors.

The purpose of analysing the prominent journals is to identify the journals that have devoted space for publications on the research theme. This study indicates the journals that are more receptive to capital budgeting research and promote the scientific knowledge on the theme.

It was observed that the articles in the BP were published in 33 different journals, while the ones from the aligned references in the BP were distributed across 49 journals.

It is observed that the prominent journal in the BP was “Financial Management” (FM) from the Financial Management Association (FMA) with six articles, and at the same tame with five articles on the BP references. The mission of FM is to significantly affect financial investigations and business practices by publishing high-quality research. FM is not a specialized journal and, therefore, it publishes papers in all finance areas quarterly.

In the BP references, the prevailing journal is “The Engineering Economist” from the Institute of Industrial Engineers (IIE) with 9 articles. In addition, there are other relevant journals in the area such as “Long Range Planning”, “Journal of Finance Economics” and “International Journal of Production Economics”, although not evident in the Figure, have published articles in the portfolio references.

4. Systematic review

The third stage of Proknow-C shows the contents of the articles in the bibliographic portfolio, which is their systematic analysis. A critical analysis of the articles is carried out using the underlying lenses of a problem. Such lenses (or perspectives) are defined by the researcher, in order to explore the research problems in capital budgeting.

4.1. Research problems in capital budgeting

A paradigm shift in corporate investment practices over the last fifty years is seen in the capital budgeting literature (Batra & Verma, 2017Batra, R., & Verma, S. (2017). Capital budgeting practices in Indian companies. IIMB Management Review, 29(1), 29-44. http://dx.doi.org/10.1016/j.iimb.2017.02.001.

http://dx.doi.org/10.1016/j.iimb.2017.02...

). Capital budget practices are defined as techniques and methods that assist in assessing the feasibility of a project (Al-Mutairi et al., 2018Al-Mutairi, A., Naser, K., Saeid, M., & McMillan, D. (2018). Capital budgeting practices by non-financial companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance, 6(1), 2-18. http://dx.doi.org/10.1080/23322039.2018.1468232.

http://dx.doi.org/10.1080/23322039.2018....

).

Research suggests that the difference between theory and practice in capital budgeting is mainly caused by the user of the practices: managers are unable to apply the practices that should be used in the analysis of investment projects (Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

). In fact, it seems that the decision makers do not have familiarity or do not know the most appropriate methods (Lazaridis, 2004Lazaridis, I. T. (2004). Capital budgeting practices: a survey in the firms in Cyprus. Journal of Small Business Management, 42(4), 427-433. http://dx.doi.org/10.1111/j.1540-627X.2004.00121.x.

http://dx.doi.org/10.1111/j.1540-627X.20...

; Brijlal & Quesada, 2009Brijlal, P., & Quesada, L. (2009). The use of capital budgeting techniques in businesses: a perspective from the Western Cape. Journal of Applied Business Research, 25(4), 37-46.; Hall & Millard, 2011Hall, J., & Millard, S. (2011). Capital budgeting practices used by selected listed South African firms. South African Journal of Economic and Management Sciences, 13(1), 85-97. http://dx.doi.org/10.4102/sajems.v13i1.200.

http://dx.doi.org/10.4102/sajems.v13i1.2...

).

There is, however, some limited evidence that company-specific conditions will influence the effectiveness of using sophisticated capital budget practices (Chatterjee et al., 2003Chatterjee, S., Wiseman, R. M., Fiegenbaum, A., & Devers, C. E. (2003). Integrating behavioural and economic concepts of risk into strategic management: the Twain Shall meet. Long Range Planning, 36(1), 61-79. http://dx.doi.org/10.1016/S0024-6301(02)00201-7.

http://dx.doi.org/10.1016/S0024-6301(02)...

). In this context, together with the characteristics of the company, the managers' profile is also considered to be impacting in capital budgeting practices (Graham & Harvey, 2002Graham, J., & Harvey, C. (2002). How do CFOs make capital budgeting and capital structure decisions? Journal of Applied Corporate Finance, 15(1), 8-23. http://dx.doi.org/10.1111/j.1745-6622.2002.tb00337.x.

http://dx.doi.org/10.1111/j.1745-6622.20...

; Brounen et al., 2004Brounen, D., Jong, A., & Koedijk, K. (2004). Corporate finance in Europe: confronting theory with practice. Financial Management, 33(4), 71-101.) and in the decision making process (Rayo et al., 2007Rayo, S., Cortés, A. M., & Sáez, J. L. (2007). Valoración empírica de las opciones de crecimiento: el caso de la Gran Empresa Española. Revista Europea de Dirección y Economía de la Empresa, 16(2), 147-166.).

In addition, factors such as cognitive ability, preferences, profile, experience function, and managerial training also affect capital budgeting decisions (Brijlal & Quesada, 2009Brijlal, P., & Quesada, L. (2009). The use of capital budgeting techniques in businesses: a perspective from the Western Cape. Journal of Applied Business Research, 25(4), 37-46.; Egbide et al., 2013Egbide, B., Uwalomwa, U., & Agbude, G. A. (2013). Capital budgeting, government policies and the performance of SMEs in Nigeria: a hypothetical case analysis. IFE PsychologIA, 21(1), 55-73.). From the theoretical problem of the use of capital budgeting practices by managers, we intend to analyze two lenses in the systemic analysis: from the perspective of managers and from the perspective of practices.

With the research problem about the gap between theory and practice in capital budgeting, systemic analysis aims to analyze the theoretical lenses (perspectives) of articles in the bibliographic portfolio according to the issues highlighted in Table 1 in order to identify gaps and opportunities for scientific improvement for the topic under study (Marafon et al., 2015Marafon, A. D., Ensslin, L., Lacerda, R. T. O., & Ensslin, S. R. (2015). The effectiveness of multi-criteria decision aid methodology. European Journal of Innovation Management, 18(1), 86-109. http://dx.doi.org/10.1108/EJIM-10-2013-0106.

http://dx.doi.org/10.1108/EJIM-10-2013-0...

). Table 1 presents the lens and the questions that will guide the analysis of the articles from each of two perspectives.

4.2. Lens # 1 managers

Capital budgeting may be used in very simple operational decisions (such as the replacement of equipment) or more complex strategies (such as building a new plant) (Leon et al., 2008Leon, F. M., Isa, M., & Kester, G. W. (2008). Capital budgeting practices of listed Indonesian companies. Asian Journal of Business and Accounting, 1(2), 175-192.). When considering the importance of the capital investment decisions, it is imperative that executives use the best techniques and tools available to assure a grounded decision (Toit & Pienaar, 2005Toit, M. J. D., & Pienaar, A. (2005). A review of the capital budgeting behaviour of large South African firms. Meditari Accountancy Research, 13(1), 19-27. http://dx.doi.org/10.1108/10222529200500002.

http://dx.doi.org/10.1108/10222529200500...

).

From that, it was observed that 14 articles characterized the managers responsible for capital budgeting, and some of them were attempts to detect a relationship with the decision-making. Only 12 papers discussed whether the questionnaire and/or interview were directed to the president, financial director, controller or treasurer (for example, Arnold & Hatzopoulos, 2000Arnold, G. C., & Hatzopoulos, P. D. (2000). The theory-practice gap in capital budgeting: evidence from the United Kingdom. Journal of Business Finance & Accounting, 27(5-6), 603-626. http://dx.doi.org/10.1111/1468-5957.00327.

http://dx.doi.org/10.1111/1468-5957.0032...

; Ryan & Ryan, 2002Ryan, P. A., & Ryan, G. P. (2002). Capital budgeting practices of the Fortune 1000: how have things changed? Journal of Business and Management, 8(4), 1-15.; Acuña et al., 2015Acuña, E., Cancino, J., Vásquez, F., Mena, P., & Sánchez, K. (2015). Practices used in estimating the cost of capital and investment appraisal in the Chilean forestry sector. Custos e Agronegocio, 11(2), 214-228.). In most cases, it was observed that the association between the capital budgeting activity or role and senior positions in the companies requires a set of specific knowledge.

However, attention should be drawn to the fact that capital budgeting is not always considered as the role of a specialist in the companies, and this role is performed by different types of professionals (such as a fiscal advisor or treasurer), according to the studies made by Pike (1988)Pike, R. H. (1988). An empirical study of the adoption of sophisticated capital budgeting practices and decision-making effectiveness. Accounting and Business Research, 18(72), 341-351. http://dx.doi.org/10.1080/00014788.1988.9729381.

http://dx.doi.org/10.1080/00014788.1988....

and Klammer (1972)Klammer, T. P. (1972). Empirical evidence of adoption of sophisticated capital budgeting techniques. The Journal of Business, 45(3), 387-397. http://dx.doi.org/10.1086/295467.

http://dx.doi.org/10.1086/295467...

. This means that a company's investments need not be designated by a specific manager, they can be decentralized to each of the areas or departments of a company. This affects the results found in the articles, since people without experience in assessing investment proposals will probably not know the techniques and procedures to be used.

With respect to the characteristics of the research participants, the prevalence of the vice-president of finance, financial director/manager, treasurer and controller was observed, and these positions are directly involved with capital budgeting decisions (for example, Gitman & Forrester, 1977Gitman, L. J., & Forrester, J. R. (1977). Survey of capital budgeting techniques used by major United States firms. Financial Management, 6(3), 66-71. http://dx.doi.org/10.2307/3665258.

http://dx.doi.org/10.2307/3665258...

; Lazaridis, 2004Lazaridis, I. T. (2004). Capital budgeting practices: a survey in the firms in Cyprus. Journal of Small Business Management, 42(4), 427-433. http://dx.doi.org/10.1111/j.1540-627X.2004.00121.x.

http://dx.doi.org/10.1111/j.1540-627X.20...

; Khamees et al., 2010Khamees, B. A., Al-Fayoumi, N., & Al-Thuneibat, A. A. (2010). Capital budgeting practices in the Jordanian industrial corporations. International Journal of Commerce and Management, 20(1), 49-63. http://dx.doi.org/10.1108/10569211011025952.

http://dx.doi.org/10.1108/10569211011025...

).

Studies indicate that professionals with higher education will likely use discounted cash flow techniques in opposition to those who have basic education (Leon et al., 2008Leon, F. M., Isa, M., & Kester, G. W. (2008). Capital budgeting practices of listed Indonesian companies. Asian Journal of Business and Accounting, 1(2), 175-192.). Managers with a Master’s in Business Administration (MBA) or a master’s degree will probably use more sophisticated practices, compared to those who do not have a degree (Graham & Harvey, 2002Graham, J., & Harvey, C. (2002). How do CFOs make capital budgeting and capital structure decisions? Journal of Applied Corporate Finance, 15(1), 8-23. http://dx.doi.org/10.1111/j.1745-6622.2002.tb00337.x.

http://dx.doi.org/10.1111/j.1745-6622.20...

; Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

; Nurullah & Kengatharan, 2015Nurullah, M., & Kengatharan, L. (2015). Capital budgeting practices: evidence from Sri Lanka. Journal of Advances in Management Research, 12(1), 55-82. http://dx.doi.org/10.1108/JAMR-01-2014-0004.

http://dx.doi.org/10.1108/JAMR-01-2014-0...

). This is because various approaches of investment appraisal are more commonly taught in engineering and MBA programmes.

By reading 7 papers that analyse the respondents, the profile of the financial manager may be observed. The person is usually over 30 years old, an accountant, has an MBA or post-graduate degree and has occupied their current position for over five years (for example, Leon et al., 2008Leon, F. M., Isa, M., & Kester, G. W. (2008). Capital budgeting practices of listed Indonesian companies. Asian Journal of Business and Accounting, 1(2), 175-192.; Hall & Millard, 2011Hall, J., & Millard, S. (2011). Capital budgeting practices used by selected listed South African firms. South African Journal of Economic and Management Sciences, 13(1), 85-97. http://dx.doi.org/10.4102/sajems.v13i1.200.

http://dx.doi.org/10.4102/sajems.v13i1.2...

; Nurullah & Kengatharan, 2015Nurullah, M., & Kengatharan, L. (2015). Capital budgeting practices: evidence from Sri Lanka. Journal of Advances in Management Research, 12(1), 55-82. http://dx.doi.org/10.1108/JAMR-01-2014-0004.

http://dx.doi.org/10.1108/JAMR-01-2014-0...

).

It was expected that the most experienced ones and those with a university degree used formal and more sophisticated practices to analyse capital budgeting, but this was not seen (Leon et al., 2008Leon, F. M., Isa, M., & Kester, G. W. (2008). Capital budgeting practices of listed Indonesian companies. Asian Journal of Business and Accounting, 1(2), 175-192.; Hall & Mutshutshu, 2013Hall, J. H., & Mutshutshu, T. (2013). Capital budgeting techniques employed by selected South African state-owned companies. Corporate Ownership and Control, 10(3), 177-187. http://dx.doi.org/10.22495/cocv10i3c1art2.

http://dx.doi.org/10.22495/cocv10i3c1art...

). According to the research conducted by Andrés et al. (2015)Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

, the use of simple practices is explained by the fact that the managers progressively accumulate a higher number of practices over time, rather than avoiding and abandoning simple practices and using only sophisticated practices. On the other hand, it may indicate the need for managers to search for other means to learn advanced methodologies to be used, in addition to the ones they learned at their university. Some courses include little or no approach about sophisticated capital budgeting practices.

For example, it is possible that teaching sophisticated capital budgeting practices is not part of the curriculum of management and engineering undergraduate courses, as the simplest and usual are usually taught. Also, it is important to explore what is the teaching of practices in universities and to verify if it matches the need and reality of professionals. Thus, in the practice of organizations, engineering professionals involved in capital budgeting should attend training courses in finance to improve their decision-making skills (Lazaridis, 2004Lazaridis, I. T. (2004). Capital budgeting practices: a survey in the firms in Cyprus. Journal of Small Business Management, 42(4), 427-433. http://dx.doi.org/10.1111/j.1540-627X.2004.00121.x.

http://dx.doi.org/10.1111/j.1540-627X.20...

; Khamees et al., 2010Khamees, B. A., Al-Fayoumi, N., & Al-Thuneibat, A. A. (2010). Capital budgeting practices in the Jordanian industrial corporations. International Journal of Commerce and Management, 20(1), 49-63. http://dx.doi.org/10.1108/10569211011025952.

http://dx.doi.org/10.1108/10569211011025...

).

In addition, the occasional success of the investment projects depends on the effort dedicated by managers throughout the company. In such cases, Bernardo et al. (2004)Bernardo, A. E., Cai, H., & Luo, J. (2004). Capital budgeting in multidivision firms: Information, agency, and incentives. Review of Financial Studies, 17(3), 739-767. http://dx.doi.org/10.1093/rfs/hhg050.

http://dx.doi.org/10.1093/rfs/hhg050...

argue that the company must institute incentives for the managers to provide actual reports and allocate resources as effectively as possible. For Maccarrone (1996)Maccarrone, P. (1996). Organizing the capital budgeting process in large firms. Management Decision, 34(6), 43-56. http://dx.doi.org/10.1108/00251749610121489.

http://dx.doi.org/10.1108/00251749610121...

, these incentive systems have important effects on the behaviour of managers, since organizational studies show that managers are influenced by how they are evaluated and rewarded. Thus, it is expected that by granting incentives for the results achieved by managers, they will be more interested in making the best and most robust evaluations of investment projects in order to leverage their incentives.

This approach allows for the observation that managers have physical and psychological characteristics that influence their perspectives and analysis in decision-making. These characteristics involves schooling, technical knowledge, experience, age, gender, and more and may be applied to capital budgeting. However, only 6 studies (for example, Khamees et al., 2010Khamees, B. A., Al-Fayoumi, N., & Al-Thuneibat, A. A. (2010). Capital budgeting practices in the Jordanian industrial corporations. International Journal of Commerce and Management, 20(1), 49-63. http://dx.doi.org/10.1108/10569211011025952.

http://dx.doi.org/10.1108/10569211011025...

; Batra & Verma, 2014Batra, R., & Verma, S. (2014). An empirical insight into different stages of capital budgeting. Global Business Review, 15(2), 339-362. http://dx.doi.org/10.1177/0972150914523588.

http://dx.doi.org/10.1177/09721509145235...

; Vecino et al., 2015Vecino, C. E., Rojas, S. C., & Munoz, Y. (2015). Capital budgeting practices in Colombia. Estudios Gerenciales, 31(134), 41-49. http://dx.doi.org/10.1016/j.estger.2014.08.002.

http://dx.doi.org/10.1016/j.estger.2014....

) evaluated the relationship between the attributes of the manager and decision-making in investments, but it did not really verify the implications of characteristics in choosing simpler or more sophisticated practices.

The values, experiences, and personalities of managers intervene with the organization's strategic choices and the success of these choices (Hambrick, 2007Hambrick, D. C. (2007). Upper echelons theory: an update. Academy of Management Review, 32(2), 334-343. http://dx.doi.org/10.5465/amr.2007.24345254.

http://dx.doi.org/10.5465/amr.2007.24345...

). Characteristics such as age, gender, education and functional experience are indicative of the underlying cognitive and affective management aspects that determine the decisions of management teams, which subsequently affect organizational performance (Bell et al., 2011Bell, S. T., Villado, A. J., Lukasik, M. A., Belau, L., & Briggs, A. L. (2011). Getting specific about demographic diversity variable and team performance relationships: a meta-analysis. Journal of Management, 37(3), 709-743. http://dx.doi.org/10.1177/0149206310365001.

http://dx.doi.org/10.1177/01492063103650...

).

4.3. Lens # 2 practices

There is a wide variety of techniques available for use by managers to assess capital budgeting projects (Gitman & Forrester, 1977Gitman, L. J., & Forrester, J. R. (1977). Survey of capital budgeting techniques used by major United States firms. Financial Management, 6(3), 66-71. http://dx.doi.org/10.2307/3665258.

http://dx.doi.org/10.2307/3665258...

; Brijlal & Quesada, 2009Brijlal, P., & Quesada, L. (2009). The use of capital budgeting techniques in businesses: a perspective from the Western Cape. Journal of Applied Business Research, 25(4), 37-46.; Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

). While some of them are theoretically superior to others, each one has its own advantages and disadvantages (Toit & Pienaar, 2005Toit, M. J. D., & Pienaar, A. (2005). A review of the capital budgeting behaviour of large South African firms. Meditari Accountancy Research, 13(1), 19-27. http://dx.doi.org/10.1108/10222529200500002.

http://dx.doi.org/10.1108/10222529200500...

). Among the most sophisticated ones are the Discounted Cash Flow (DCF), Net Present Value (NPV) and Internal Rate of Return (IRR), and the simpler ones include the Payback (Pike, 1988Pike, R. H. (1988). An empirical study of the adoption of sophisticated capital budgeting practices and decision-making effectiveness. Accounting and Business Research, 18(72), 341-351. http://dx.doi.org/10.1080/00014788.1988.9729381.

http://dx.doi.org/10.1080/00014788.1988....

).

Within that context, the capital budgeting practices were explored by 29 articles from the bibliographic portfolio (BP). From that total, 27 evaluated the techniques that managers used (93.10%) and 2 (6.90%) verified the evolution of the techniques using data from longitudinal studies.

With respect to the assessment, discount rate and risk analysis practices, it was observed that Payback was used in thirteen studies, Weighted Average Cost of Capital (WACC) in eight studies, and Sensitivity Analysis (SA) in eleven, respectively. Furthermore, the less frequently used techniques by managers to assess investment projects were Net Present Value (NPV) (for example, Pike, 1983Pike, R. H. (1983). A review of recent trends in formal capital budgeting processes. Accounting and Business Research, 13(51), 201-208. http://dx.doi.org/10.1080/00014788.1983.9729753.

http://dx.doi.org/10.1080/00014788.1983....

, 1984Pike, R. H. (1984). Sophisticated capital budgeting systems and their association with corporate performance. Managerial and Decision Economics, 5(2), 91-97. http://dx.doi.org/10.1002/mde.4090050207.

http://dx.doi.org/10.1002/mde.4090050207...

, 1986Pike, R. H. (1986). The design of capital-budgeting processes and the corporate context. Managerial and Decision Economics, 7(3), 187-195. http://dx.doi.org/10.1002/mde.4090070307.

http://dx.doi.org/10.1002/mde.4090070307...

) and the Decision Tree (DT) (for example, Ryan & Ryan, 2002Ryan, P. A., & Ryan, G. P. (2002). Capital budgeting practices of the Fortune 1000: how have things changed? Journal of Business and Management, 8(4), 1-15.; Lazaridis, 2004Lazaridis, I. T. (2004). Capital budgeting practices: a survey in the firms in Cyprus. Journal of Small Business Management, 42(4), 427-433. http://dx.doi.org/10.1111/j.1540-627X.2004.00121.x.

http://dx.doi.org/10.1111/j.1540-627X.20...

; Hall & Mutshutshu, 2013Hall, J. H., & Mutshutshu, T. (2013). Capital budgeting techniques employed by selected South African state-owned companies. Corporate Ownership and Control, 10(3), 177-187. http://dx.doi.org/10.22495/cocv10i3c1art2.

http://dx.doi.org/10.22495/cocv10i3c1art...

).

Payback is not a desirable investment criterion, since it ignores the value of money throughout time and the value of cash flows beyond the cutting date (Pike, 1983Pike, R. H. (1983). A review of recent trends in formal capital budgeting processes. Accounting and Business Research, 13(51), 201-208. http://dx.doi.org/10.1080/00014788.1983.9729753.

http://dx.doi.org/10.1080/00014788.1983....

; Graham & Harvey, 2002Graham, J., & Harvey, C. (2002). How do CFOs make capital budgeting and capital structure decisions? Journal of Applied Corporate Finance, 15(1), 8-23. http://dx.doi.org/10.1111/j.1745-6622.2002.tb00337.x.

http://dx.doi.org/10.1111/j.1745-6622.20...

; Egbide et al., 2013Egbide, B., Uwalomwa, U., & Agbude, G. A. (2013). Capital budgeting, government policies and the performance of SMEs in Nigeria: a hypothetical case analysis. IFE PsychologIA, 21(1), 55-73.). Despite the fragilities indicated in the academic literature, how should the persistence of the technique be explained? In that sense, in the 27 papers that were analysed, it was observed that only 12 justified their choice of the techniques used. This means that several of them (approximately 55.5%) only conducted a descriptive diagnosis through a survey.

Managers have argued that they use Payback because it is easier to calculate, understand and compare (to a percentage return) than an absolute cash increase in the wealth of stakeholders (for example, Ryan & Ryan, 2002Ryan, P. A., & Ryan, G. P. (2002). Capital budgeting practices of the Fortune 1000: how have things changed? Journal of Business and Management, 8(4), 1-15.; Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

).

Other authors defend that the explanation may be attributed to the lack of financial sophistication of managers (Ryan & Ryan, 2002Ryan, P. A., & Ryan, G. P. (2002). Capital budgeting practices of the Fortune 1000: how have things changed? Journal of Business and Management, 8(4), 1-15.; Hall & Millard, 2011Hall, J., & Millard, S. (2011). Capital budgeting practices used by selected listed South African firms. South African Journal of Economic and Management Sciences, 13(1), 85-97. http://dx.doi.org/10.4102/sajems.v13i1.200.

http://dx.doi.org/10.4102/sajems.v13i1.2...

); the limited use of the computer technology (Pike, 1988Pike, R. H. (1988). An empirical study of the adoption of sophisticated capital budgeting practices and decision-making effectiveness. Accounting and Business Research, 18(72), 341-351. http://dx.doi.org/10.1080/00014788.1988.9729381.

http://dx.doi.org/10.1080/00014788.1988....

, 1996Pike, R. H. (1996). A longitudinal survey on capital budgeting practices. Journal of Business Finance & Accounting, 23(1), 79-92. http://dx.doi.org/10.1111/j.1468-5957.1996.tb00403.x.

http://dx.doi.org/10.1111/j.1468-5957.19...

; Ryan & Ryan, 2002Ryan, P. A., & Ryan, G. P. (2002). Capital budgeting practices of the Fortune 1000: how have things changed? Journal of Business and Management, 8(4), 1-15.; Hall & Millard, 2011Hall, J., & Millard, S. (2011). Capital budgeting practices used by selected listed South African firms. South African Journal of Economic and Management Sciences, 13(1), 85-97. http://dx.doi.org/10.4102/sajems.v13i1.200.

http://dx.doi.org/10.4102/sajems.v13i1.2...

); the lack of familiarity with the most sophisticated methods (Graham & Harvey, 2002Graham, J., & Harvey, C. (2002). How do CFOs make capital budgeting and capital structure decisions? Journal of Applied Corporate Finance, 15(1), 8-23. http://dx.doi.org/10.1111/j.1745-6622.2002.tb00337.x.

http://dx.doi.org/10.1111/j.1745-6622.20...

; Lazaridis, 2004Lazaridis, I. T. (2004). Capital budgeting practices: a survey in the firms in Cyprus. Journal of Small Business Management, 42(4), 427-433. http://dx.doi.org/10.1111/j.1540-627X.2004.00121.x.

http://dx.doi.org/10.1111/j.1540-627X.20...

; Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

); the lack of personnel, time and experience (Khamees et al., 2010Khamees, B. A., Al-Fayoumi, N., & Al-Thuneibat, A. A. (2010). Capital budgeting practices in the Jordanian industrial corporations. International Journal of Commerce and Management, 20(1), 49-63. http://dx.doi.org/10.1108/10569211011025952.

http://dx.doi.org/10.1108/10569211011025...

) and the use as a secondary method to support the main method (Toit & Pienaar, 2005Toit, M. J. D., & Pienaar, A. (2005). A review of the capital budgeting behaviour of large South African firms. Meditari Accountancy Research, 13(1), 19-27. http://dx.doi.org/10.1108/10222529200500002.

http://dx.doi.org/10.1108/10222529200500...

; Brijlal & Quesada, 2009Brijlal, P., & Quesada, L. (2009). The use of capital budgeting techniques in businesses: a perspective from the Western Cape. Journal of Applied Business Research, 25(4), 37-46.).

One of the developments over the past decade has been real options. After all, most of the capital investment projects have options (Bennouna et al., 2010Bennouna, K., Meredith, G. G., & Marchant, T. (2010). Improved capital budgeting decision making: evidence from Canada. Management Decision, 48(2), 225-247. http://dx.doi.org/10.1108/00251741011022590.

http://dx.doi.org/10.1108/00251741011022...

). Some research showed the limited use of such a technique (for example, Graham & Harvey, 2002Graham, J., & Harvey, C. (2002). How do CFOs make capital budgeting and capital structure decisions? Journal of Applied Corporate Finance, 15(1), 8-23. http://dx.doi.org/10.1111/j.1745-6622.2002.tb00337.x.

http://dx.doi.org/10.1111/j.1745-6622.20...

; Hall & Mutshutshu, 2013Hall, J. H., & Mutshutshu, T. (2013). Capital budgeting techniques employed by selected South African state-owned companies. Corporate Ownership and Control, 10(3), 177-187. http://dx.doi.org/10.22495/cocv10i3c1art2.

http://dx.doi.org/10.22495/cocv10i3c1art...

). Research with financial resources evidence the real options stand behind almost every other capital budgeting practices in terms of popularity in the corporate world (Baker et al., 2011Baker, H. K., Dutta, S., & Saadi, S. (2011). Management views on real options in capital budgeting. Journal of Applied Finance, 21(1), 18-29.; Ryan & Ryan, 2002Ryan, P. A., & Ryan, G. P. (2002). Capital budgeting practices of the Fortune 1000: how have things changed? Journal of Business and Management, 8(4), 1-15.). Managers with an MBA are less likely to know real options compared to those with non-MBA masters. Among non-users familiar with real options, the complexity of techniques is the biggest obstacle to implementation (Horn et al., 2015Horn, A., Kjærland, F., Molnár, P., & Steen, B. W. (2015). The use of real option theory in Scandinavia’s largest companies. International Review of Financial Analysis, 41, 74-81. http://dx.doi.org/10.1016/j.irfa.2015.05.026.

http://dx.doi.org/10.1016/j.irfa.2015.05...

). Nevertheless, it identifies the opportunities to explore the use of advanced and current techniques, which have been rarely analyzed in portfolio articles.

Decisions such as support simulation techniques, linear programming and sensitivity analysis were applied to the capital budgeting literature to assist the decision-maker to address the inherent uncertainty of future events (Northcott, 1991Northcott, D. (1991). Rationality and decision making in capital budgeting. The British Accounting Review, 23(3), 219-233. http://dx.doi.org/10.1016/0890-8389(91)90083-E.

http://dx.doi.org/10.1016/0890-8389(91)9...

). However, strengthening the use of such methods seems to be even higher because they tend to be used in connection with other different tools (Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

). Again, there is the need for the professional training of managers and analysts. This is necessary to promote the replacement of less advanced techniques and encourage the adoption of more accurate techniques (Hall & Mutshutshu, 2013Hall, J. H., & Mutshutshu, T. (2013). Capital budgeting techniques employed by selected South African state-owned companies. Corporate Ownership and Control, 10(3), 177-187. http://dx.doi.org/10.22495/cocv10i3c1art2.

http://dx.doi.org/10.22495/cocv10i3c1art...

).

Amid these findings, it is necessary to state that there is not a single and exhaustive method used in capital budgeting analysis. In contrast, there is the need to use several methods, preferably a combination of simple and sophisticated methods. Regardless of that, it was observed that the central factor that serves as the basis for the decisions made by the managers in the studies are the physical and psychological aspects. However, it is noteworthy that the organizational structure was indicated by Lazaridis (2004)Lazaridis, I. T. (2004). Capital budgeting practices: a survey in the firms in Cyprus. Journal of Small Business Management, 42(4), 427-433. http://dx.doi.org/10.1111/j.1540-627X.2004.00121.x.

http://dx.doi.org/10.1111/j.1540-627X.20...

and Brijlal & Quesada (2009)Brijlal, P., & Quesada, L. (2009). The use of capital budgeting techniques in businesses: a perspective from the Western Cape. Journal of Applied Business Research, 25(4), 37-46. and the behaviour of the manager by Maccarrone (1996)Maccarrone, P. (1996). Organizing the capital budgeting process in large firms. Management Decision, 34(6), 43-56. http://dx.doi.org/10.1108/00251749610121489.

http://dx.doi.org/10.1108/00251749610121...

as justifications for the choices made by the decision-makers.

This indicates that it is healthy to consider the influence and biases of managers in making capital budgeting decisions, as it has been found that their characteristics influence the use of sophisticated and or traditional practices. It is suggested that the consideration of managers' predispositions will allow a better prediction of the results of evaluations of companies' investment projects, by means of their area of education, age, investment profile, gender, level of education, for example.

4.4. Main contributions

Previous empirical investigations can be classified into two main subjects. In the first, researchers looked into investment appraisal techniques most frequently used in practice. In the second, researches attempted to establish a relationship between the use of specific investment appraisal techniques and the firm.

In the first subject, some researches on this approach were motivated due to the gap between theory and practice and, for this reason, an empirical research was conducted in order to observe the situation of the use of capital budgeting. For this purpose, a survey-based research was conducted with the use of questionnaires. On the data examination, some researchers conducted a statistical treatment (for example, Pike, 1988Pike, R. H. (1988). An empirical study of the adoption of sophisticated capital budgeting practices and decision-making effectiveness. Accounting and Business Research, 18(72), 341-351. http://dx.doi.org/10.1080/00014788.1988.9729381.

http://dx.doi.org/10.1080/00014788.1988....

, 1989Pike, R. H. (1989). Do sophisticated capital budgeting approaches improve investment decision-making effectiveness? The Engineering Economist, 34(2), 149-161. http://dx.doi.org/10.1080/00137918908902983.

http://dx.doi.org/10.1080/00137918908902...

, 1996Pike, R. H. (1996). A longitudinal survey on capital budgeting practices. Journal of Business Finance & Accounting, 23(1), 79-92. http://dx.doi.org/10.1111/j.1468-5957.1996.tb00403.x.

http://dx.doi.org/10.1111/j.1468-5957.19...

; Andrés et al., 2015Andrés, P., Fuente, G., & San Martín, P. (2015). Capital budgeting practices in Spain. Business Research Quarterly, 18(1), 37-56. http://dx.doi.org/10.1016/j.brq.2014.08.002.

http://dx.doi.org/10.1016/j.brq.2014.08....

), other conducted only a descriptive analysis (for example, Gitman & Forrester, 1977Gitman, L. J., & Forrester, J. R. (1977). Survey of capital budgeting techniques used by major United States firms. Financial Management, 6(3), 66-71. http://dx.doi.org/10.2307/3665258.

http://dx.doi.org/10.2307/3665258...

; Bennouna et al., 2010Bennouna, K., Meredith, G. G., & Marchant, T. (2010). Improved capital budgeting decision making: evidence from Canada. Management Decision, 48(2), 225-247. http://dx.doi.org/10.1108/00251741011022590.

http://dx.doi.org/10.1108/00251741011022...

). On these papers, the general purpose is to diagnose how the use of capital budgeting occurs or which practices are more and less used. However, only descriptive analyzes were made on the use of capital budgeting practices. The authors did not explore the relationship of practices with return on investment or company performance. Thus, it is not possible to ascertain what greater or lesser use of a practice may imply.

In the second subject, most papers involved companies located in the United Kingdom, Sweden, Poland, Cyprus, United States, Canada and Spain. It is possible to observe the existence of studies in emerging countries such as South Africa, India, Indonesia and Jordan, with the justification that studies related to knowledge on capital budgeting in emerging economies are still limited. The focus on company samples that act on structured, consolidated and developing markets may be observed. Additionally, some authors use as reference a set of companies from lists such as Fortune 100, Times 1000, Compustat and from specific stock exchanges. The prevalence of large private companies and companies from the industrial sector is highlighted. It was also observed the development of studies involving small, medium and large-sized companies (Arnold & Hatzopoulos, 2000Arnold, G. C., & Hatzopoulos, P. D. (2000). The theory-practice gap in capital budgeting: evidence from the United Kingdom. Journal of Business Finance & Accounting, 27(5-6), 603-626. http://dx.doi.org/10.1111/1468-5957.00327.

http://dx.doi.org/10.1111/1468-5957.0032...

; Brijlal & Quesada, 2009Brijlal, P., & Quesada, L. (2009). The use of capital budgeting techniques in businesses: a perspective from the Western Cape. Journal of Applied Business Research, 25(4), 37-46.; Egbide et al., 2013Egbide, B., Uwalomwa, U., & Agbude, G. A. (2013). Capital budgeting, government policies and the performance of SMEs in Nigeria: a hypothetical case analysis. IFE PsychologIA, 21(1), 55-73.) and state-owned and private companies (Sandahl & Sjögren, 2003Sandahl, G., & Sjögren, S. (2003). Capital budgeting methods among Sweden’s largest groups of companies: the state of the art and a comparison with earlier studies. International Journal of Production Economics, 84(1), 51-69. http://dx.doi.org/10.1016/S0925-5273(02)00379-1.

http://dx.doi.org/10.1016/S0925-5273(02)...

; Hall & Mutshutshu, 2013Hall, J. H., & Mutshutshu, T. (2013). Capital budgeting techniques employed by selected South African state-owned companies. Corporate Ownership and Control, 10(3), 177-187. http://dx.doi.org/10.22495/cocv10i3c1art2.

http://dx.doi.org/10.22495/cocv10i3c1art...

), in such a way as to find relationships, similarities or differences among these sizes and types of organizations. However, the analysis of different types and sizes of companies is still quite superficial. There is no regression model analysis to verify the positive and negative relationships of firm characteristics in simple or sophisticated capital budgeting practices.

In addition, there are articles with theoretical approach goes beyond building an overview of capital budgeting, it tries to understand it. Some researches tries to compare the theory and the development of the practice through the positioning of the manager (Mao, 1970Mao, J. C. T. (1970). Survey of capital budgeting: theory and practice. The Journal of Finance, 25(2), 349-360. http://dx.doi.org/10.1111/j.1540-6261.1970.tb00513.x.

http://dx.doi.org/10.1111/j.1540-6261.19...

; Pike, 1983Pike, R. H. (1983). A review of recent trends in formal capital budgeting processes. Accounting and Business Research, 13(51), 201-208. http://dx.doi.org/10.1080/00014788.1983.9729753.

http://dx.doi.org/10.1080/00014788.1983....

); to relate the use of practices to the corporate context (Pike, 1986Pike, R. H. (1986). The design of capital-budgeting processes and the corporate context. Managerial and Decision Economics, 7(3), 187-195. http://dx.doi.org/10.1002/mde.4090070307.

http://dx.doi.org/10.1002/mde.4090070307...

); and to understand the positioning of the managers under the perspective of behavioral finances (Statman & Caldwell, 1987Statman, M., & Caldwell, D. (1987). Applying behavioral finance to capital budgeting: project terminations. Financial Management, 16(4), 7-15. http://dx.doi.org/10.2307/3666103.

http://dx.doi.org/10.2307/3666103...

); and under the perspective of rationality (Northcott, 1991Northcott, D. (1991). Rationality and decision making in capital budgeting. The British Accounting Review, 23(3), 219-233. http://dx.doi.org/10.1016/0890-8389(91)90083-E.

http://dx.doi.org/10.1016/0890-8389(91)9...